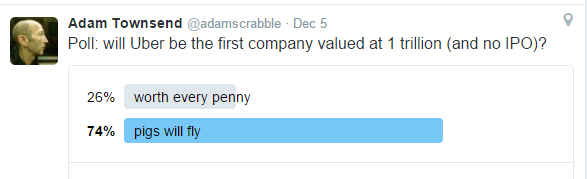

Is Uber properly valued, without qualifying your answer, Yes or No?

Uber has an assumed valuation of 92 billion billion dollars. With today’s mega valuation that may seem in line and compares favorably to its peers, or it may not. We don’t know.

There is very little known of the underlying component earnings of Uber. There are some leaked gross numbers that mysteriously appeared in Business Insider two years ago and we may have anecdotal commentary on the service, but is it worth its valuation of 92 billion dollars and the almost 10 billion dollars it has raised in 13 ever increasing rounds?

Uber is a lottery ticket, not that much different than the convenient type you can buy locally. Are you willing to buy that ticket? It must continue to rise in value and it must have liquidity for the ticket to pay off.

The valuation has changed from some unknown multiple of its growth as a taxi dispatcher and algorithm possessor to a precurser of the robotic taxi driver in The Fifth Element. Maybe that will make sense, people don’t need new cars, those purchases have been made with ‘future dollars’ that are being spent ‘today’ via the Fed having pushed the consumer to action.

Uber’s dream is wondrous, like an HG Wells story, but peoples behavior has to change and that is multi-generational, enormous government spending has to occur, laws have to be changed, robot ethics have to be philosophized, interest rates have to be favorable and the debt markets have to be willing to buy in a ruthless market.

Funding this and other Unicorns includes State and City pensions funds that have dramatically increased allocations to venture capital over the past several years as they need to meet the obligations of decades of politicians that committed the future to get union endorsements. This while LP’s like myself have reduced our exposure and retreated to family offices that can invest more precisely

Entitlements obligations are a staggering burden and it pushes the pensions to make extraordinary bets.

Last month Calpers after years of lawsuits and challenges finally revealed its payout to private equity and venture capital firms. It was a staggering transfer of wealth from the Calpers pensioners to venture firms. Investments into venture capital yielded returns below the high water mark for the asset class. And, the last tranche of their investments will likely have a significantly lesser return as liquidity events and IPO’s becoming scarcer.

That type of dismal return indicates aggresive churning of the money, excessive reliance on placement agents and a failed blind pool strategy that invests in sectors, pension don’t know what they are buying. This might have been an acceptable investment ‘style’ when the dollars were smaller, but it is a hard to manage risk and hedge when the dollars are huge.

Payouts to the pensioners have to occur on schedule and the guarantee if not satisfied by the performance of the funds comes from taxpayers in one way, shape or form. There are a lot of buckets that the state and cities can pilfer from, but they are all ‘ours’, the taxpayers.

Whether you agree with the Fed’s likely move to phase in increased rates, it will happen and it will create ripples. Money that should be available to startups is instead being hoarded by Unicorns.

By manafacturing Unicorns, Venture Capital firms have created a generation of annuities on the carry that does not get distributed to the LP’s.

The Fed does not intervene in quality or quantitative decisions of how the money they created is spent. It is charged with affecting employment and supply and demand and that intention has been corrupted by pricing Uber in the backrooms with no visibility, no reporting.

Companies that are the recipient of staggering amounts of capital should have to make public reports should be regulated aggressively by the SEC rather than the self policing and arguable trickle down economics that VC firms now enjoy.

Uber, and many of its peers may be mythological and a lottery ticket that you fractionally own.