This post is part of a series of essays about currency and “the dollar” and this one is to equip you for battle against who talk about how America should ideally return to a gold standard, and so on.

I’ve heard many people say “gold standard” and reminisce about a past without having had the misery to have lived in it.

“GOLD STANDARD” sounds smart and has a world weary cynicism that can be convincing to the easily convinced. These people will show charts without context and do economic sleight of hand. I want to equip you with the information so that you can economically beat them up.

Let’s begin…

Many people feel that American prosperity started its decline on Aug. 15, 1971 the day that…

Nixon eliminated the gold standard

…a monetary system in which dollars were backed by and could be exchanged for a fixed amount of gold.

Since then, the United States has used a fiat currency, in which dollars are valuable simply because the government says they are.

The term “fiat” is derived from the Latin fieri, meaning an arbitrary act or decree. In keeping with this etymology, the value of fiat currencies is ultimately based on the fact that they are defined as legal tender by way of government decree.

Why doesn’t the U.S. return to the gold standard so that the Fed can’t “create money out of thin air” referring to the Fed’s ability to create money at virtually zero resource cost. It is frequently asserted that such an ability necessarily leads to “too much” price inflation.

Under a gold standard, the temptation to overinflate is allegedly absent, that is, gold cannot be “created out of thin air.” It would follow that a return to a gold standard would be the only way to guarantee price-level stability and spending constraints.

Before we can look at contemporary theories on a gold standard we have to do a quick, incomplete, retrospective on ‘what happened’ before.

The gold standard Great Depression

The gold standard was a global arrangement that formed the basis for a virtually universal fixed-exchange rate regime in which international transactions were settled in gold.

The length and depth of the deflation during the late 1920s and early 1930s strongly suggest a monetary origin...

This meant that a country with an external deficit, one whose imports exceed its exports, was required to pay the difference by transferring gold to countries with external surpluses.

The loss of gold forced the deficit country’s central bank to shrink its balance sheet, reducing the quantity of money and credit in the economy, and driving domestic prices down.

Put differently, under a gold standard, countries running external deficits face deflationary pressure. A surplus country’s central bank faced no such pressure, as it could choose whether to convert higher gold stocks into money or not.

The result was catastrophic, compelling deficit countries with gold outflows to tighten their monetary policies even more. As the quantity of money available worldwide shrank, so did the price level, adding to the real burden of debt, and prompting defaults and bank failures virtually around the world.

Imagine how bad it would be now, America has a deficit of almost $1 trillion dollars a year against China alone, now add Korea, Mexico and so on, all big deficits for America. Not fun, we would be crushed, and they would be too,

Implementing a gold standard

The idealized gold standard possesses

- automaticity

- stability

- self-correcting mechanisms

- minimal human intervention

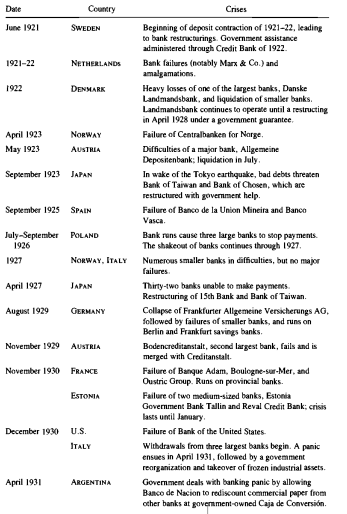

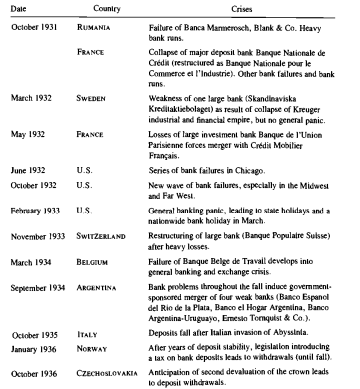

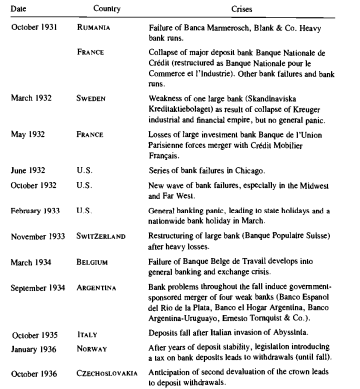

The actual gold standard only was in force from the 1870s to 1914, and briefly between the two world wars. The former period was the Great Depression and the latter period was a Great(er) Depression that exceeded it in depth, severity and contagion.

There is a breadth of theories of a contemporary gold standard, too many and intricate for this post, but I will lay out the conditions for the two primary strategies from which the theories derive.

Gold backing without convertibility

…limits the growth in the supply of money

The most limited proposal for gold backing calls for stipulating that the currency in circulation must be backed by the existing official gold stock of the United States at a current official price of $xyz an ounce, and that the allowable growth in outstanding currency should be limited to around 3% a year after a transition period, assured by revaluing the existing gold stock by an equal measure of 3% a year.

This is a proposal that is just a monetary rule in that gold plays no essential role.

Because this is inadequate it won’t be discussed further but we can expand and introduce new features: Gold backing for all or some portion of the money supply could also be required at a fixed price of gold, or at the market price of gold, which fluctuates substantially.

If the gold backing requirement does not bind, that is, if the value of the monetary gold exceeds the requirement for gold reserves, we would be in the realm of discretionary monetary policy, as we are now.

When the reserve requirement does bind, the monetary authorities would have to buy gold in order to increase the money supply. Unlike under a regime of convertibility, the purchase would be at the discretion of the monetary authorities. As we are now.

This kind of arrangement poses difficult but not insuperable technical problems over the valuation of monetary gold but the key point is that this would be a discretionary regime, not an automatic one, unless in addition a rule governing monetary growth were also imposed.

Gold backing by itself does not provide monetary discipline. The United States had backing for many years, and during most of that period the gold reserve requirements were not binding.

Gold Convertibility

Proposals involving convertibility vary, some calling in effect for full convertibility of all Federal Reserve notes and 100 percent gold money thereafter.

Bank notes could be issued by private banks, but they would in effect be depository receipts for gold.

Although the modus operandi would vary substantially from one proposal to another, the underlying idea is the same: whenever some substantial group of dollar holders became dissatisfied with monetary developments and unsure about the future value of the dollar, they could and presumably would convert their dollars to gold.

These conversions in turn would require the Federal Reserve to defend its gold reserves by tightening credit conditions or otherwise persuading the relevant public that gold conversions were unwarranted.

The system in principle would be symmetrical:

- as gold reserves increased, the money supply would expand; this feature has not been emphasized by most proponents of gold convertibility. Moreover, historically central banks have often offset (“sterilized”) the expansionary effects of gold inflows, as the United States did during the late 1930s and again during the late 1940s

- Sterilization is not possible when gold (or gold certificates) is the sole form of money. Since new gold production is small relative to outstanding gold stocks, the requirement for convertibility, it is argued, will automatically limit the rate of money creation, hence inflation, since there is a natural limit to how rapidly gold reserves can grow. Too rapid monetary growth would lead to conversion, which in turn (to preserve convertibility) would necessitate monetary retrenchment.

One difficulty with the credibility of a requirement for convertibility of U.S. dollars into gold is the already huge volume of liquid dollar assets around the world. Full convertibility would hardly be credible, given the relation of assets to potential claims.

Of course, not all outstanding liquid dollar claims would formally be convertible into gold; presumably the convertibility requirement would strictly apply only to Federal Reserve liabilities. But that provides no comfort, since the financial system functions on the supposition that all liquid dollar claims can, on short notice, be converted into claims on the Federal Reserve, either federal funds or currency. To deny or repudiate this more general convertibility is tantamount to a breakdown in the financial system, both domestic and international.

Moreover, a major strength of the international financial system at present is that for large holders (that is, leaving aside bank notes) it is a closed system, so funds can be moved around in it but cannot be withdrawn from it, except by the Federal Reserve System.

This feature served the international economy well in “recycling” the large trade surpluses, and large trade deficits. It would be altered by gold convertibility, which would provide a potential leakage to the system at the initiative of dollar holders, and thus could threaten the system as a whole with a convertibility crisis, as in 1931.

There is another disadvantage to reinstituting gold:

The principal producers of gold in the world, together accounting for nearly 80 percent of world production, are South Africa and Russia.

Both countries are, in very different ways, at political odds with other members of the community of nations. Restoring gold convertibility would provide a windfall of considerable magnitude to those two countries. They could sell all they wished without depressing the market and would place the monetary system of the United States hostage to the political decisions in one or both of these countries.

No Escape from discretion

The choice of a price for gold plays a central role in the viability of any restoration of gold to a monetary role. Yet the choice of a price, while crucial, is unavoidably arbitrary and is known to be arbitrary. So long as this is so, a rule based on a supposedly fixed price of gold cannot be a credible rule.

If gold were to become unduly constraining, its price could be changed

It is intrinsic to the process of setting a price in the first place. In this respect, the situation today is fundamentally different from the situation in the nineteenth and early twentieth centuries. Then the dollar price of gold was historically given and not open to question (except for minor adjustments on several occasions to preserve the relation to silver).

The price was not conceived as a policy variable. Now it must be.

Gold ceases to provide monetary discipline if its price can be varied.

So long as the price of gold is a policy variable, a gold standard cannot be a credible disciplinarian. It provides no escape from the need for human management, however frail that may seem to be.

Conclusion

A gold standard is not a guarantee of price stability. It is simply a promise made “out of thin air” to keep the supply of money anchored to the supply of gold.

Ultimately, money, whatever it is, even bitcoin, is a social convention.

The end?